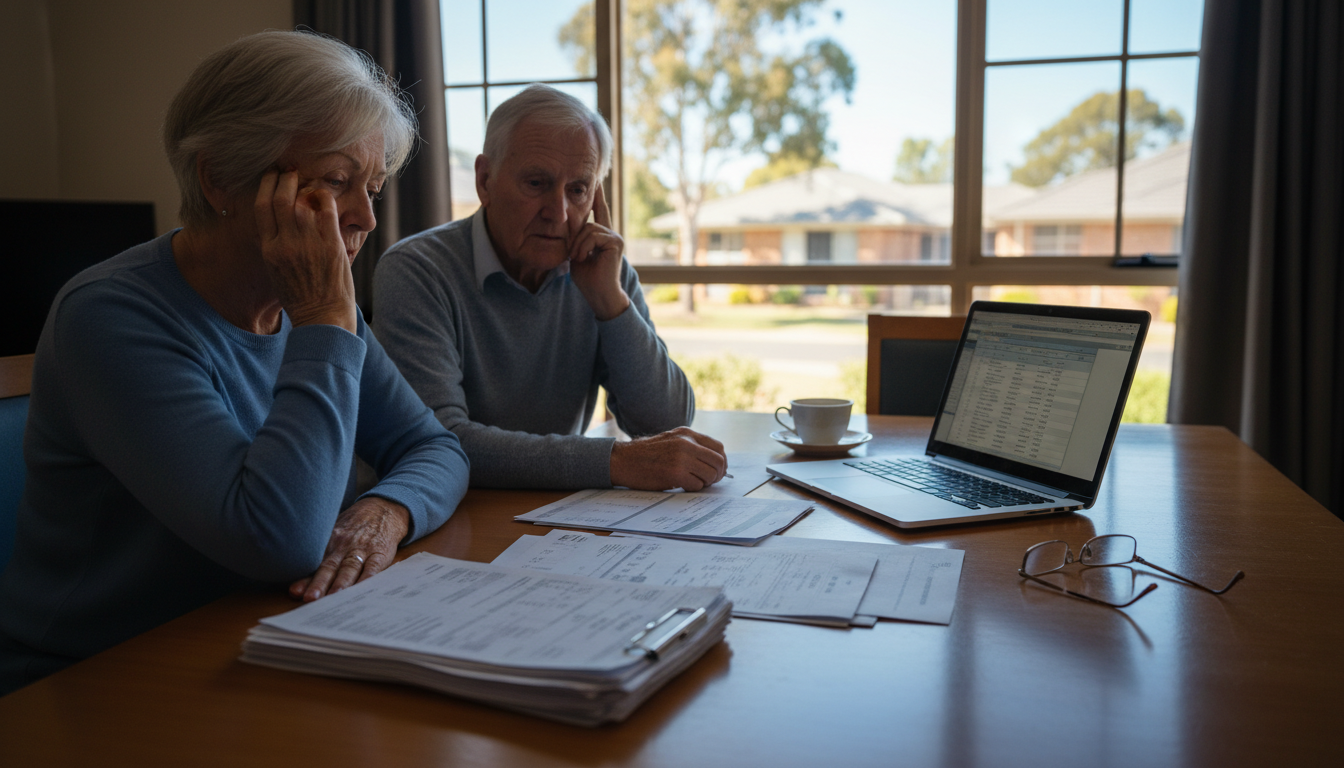

When you or a loved one needs aged care in Australia, the financial side can seem very confusing. Many people worry about the potential for an aged care financial drain on their assets and what this might mean for their inheritance. This guide helps you understand the different parts of the aged care finance system.

Key Takeaways

- Aged care costs involve various fees, including the Refundable Accommodation Deposit (RAD) and ongoing daily charges.

- The RAD can be a large sum, often hundreds of thousands of dollars, which many pay by selling assets.

- Means-testing determines your contribution to care costs based on your income and assets.

- Many perceive the system as designed to deplete assets, leading to concerns about inheritance.

- Careful financial planning is important to manage these costs.

The Complexity of Aged Care Costs

Entering aged care involves understanding a range of fees and charges. It is not a simple, flat fee. Instead, the costs are made up of several components that depend on your financial situation and the type of care you receive. This complexity often makes families feel overwhelmed and unsure of how to plan.

Your financial contributions to aged care can include:

- Accommodation costs: These cover your room and living expenses.

- Care costs: These are for the personal and nursing care you receive.

- Basic daily fees: A standard fee paid by everyone.

- Means-tested care fees: An additional fee based on your income and assets.

- Extra service fees: Charges for additional services or amenities offered by the facility.

Refundable Accommodation Deposit (RAD) Explained

One of the largest components of aged care costs is the Refundable Accommodation Deposit (RAD). This is a lump-sum payment for your room in an aged care facility. It is important to know that the RAD is just that-refundable. When you leave the facility, the RAD is paid back to you or your estate, minus any agreed deductions.

However, the size of the RAD can be substantial. For desirable rooms in many facilities, the RAD can often exceed $800,000, and sometimes even reach $1 million or more. This significant amount often requires people to sell their family home or draw down on superannuation to pay it. While the RAD is refundable, critics argue that the system encourages people to liquidate major assets without offering a substantial return on this deposit during their stay.

Daily Accommodation Payment (DAP) and Other Fees

If you cannot or choose not to pay the full RAD, you have the option to pay a Daily Accommodation Payment (DAP). The DAP is an interest-based payment calculated on the unpaid portion of the RAD. This means if your RAD is $800,000 and you only pay $400,000 as a lump sum, you will pay a daily interest amount on the remaining $400,000.

Beyond the accommodation costs (RAD or DAP), you will also pay ongoing daily fees:

- Basic Daily Fee: This is a standard fee paid by everyone receiving residential aged care. It is set at a percentage of the single basic age pension. This fee covers daily living expenses like meals, cleaning, and laundry.

- Means-Tested Care Fee: This fee is an additional contribution towards the cost of your care. It is calculated by the government based on an assessment of your income and assets. The more income and assets you have above certain thresholds, the higher your means-tested care fee will be, up to a yearly and lifetime cap.

These ongoing fees, especially the basic daily fee and the means-tested care fee, are often seen as a constant financial drain. They continue for the duration of your stay, ensuring that your financial resources are continually drawn upon.

Understanding Means-Testing and Its Impact

Means-testing is a government process that assesses your income and assets to determine how much you need to contribute to your aged care costs. This assessment looks at:

- Your income: This includes pensions, superannuation income streams, and any other regular income.

- Your assets: This includes your home (with some exemptions), savings, investments, and other property.

The assessment results in a combined income and assets figure. If this figure is above certain thresholds, you will be required to pay a means-tested care fee. The purpose of means-testing is to ensure that those with greater financial capacity contribute more to their care. However, for many families, the assessment process can be opaque, and the resulting fees can be substantial, contributing to the perception of asset depletion.

The rules around means-testing can be difficult to follow. This is why many families seek professional financial advice to understand how their assets and income will be assessed and what strategies might be available to manage these costs.

The Perceived Predatory Nature of the System

Many individuals and families view the aged care financing structure with concern, often seeing it as a "rort" or a system designed to deplete assets and inheritance. This perception arises from several factors:

- High RADs: The large lump sums required for RADs often necessitate selling the family home or drawing down superannuation.

- Ongoing Fees: The combination of basic daily fees and means-tested care fees creates a continuous outflow of money.

- Lack of Return: While the RAD is refundable, it does not earn interest, meaning the capital is tied up without growth.

- Complexity: The intricate rules around RADs, DAPs, means-testing, and various fees make it hard for the average person to fully grasp the financial implications.

These factors combine to create a feeling that the system encourages people to liquidate their assets, only for those assets to be gradually consumed by ongoing fees until financial resources are exhausted or the person passes away. This can leave little or nothing for inheritance, which is a significant concern for many families.

Protecting Your Assets and Inheritance

Given the complexities and potential for an aged care financial drain, planning is very important. While the system is designed to have individuals contribute to their care based on their means, there are legal and ethical ways to manage your financial situation.

Consider these steps:

- Seek financial advice: A specialist in aged care finance can help you understand your options and plan for costs.

- Understand the rules: Learn about RADs, DAPs, and how means-testing works.

- Review your assets: Understand how your home, superannuation, and other investments will be treated in the assessment.

- Consider payment options: Decide if a lump-sum RAD, DAP, or a combination is best for your situation.

For organizations managing aged care, understanding the regulatory landscape is paramount. Effective aged care compliance software can assist providers in managing their financial and operational obligations, ensuring transparency and adherence to government guidelines. This in turn can help families feel more confident in the system.

Frequently Asked Questions

What is the difference between a RAD and a DAP?

A RAD (Refundable Accommodation Deposit) is a lump-sum payment for your aged care room, which is refunded when you leave. A DAP (Daily Accommodation Payment) is a daily interest payment if you choose not to pay the full RAD upfront.

How is the Means-Tested Care Fee calculated?

The Means-Tested Care Fee is calculated by the government based on an assessment of your income and assets. It is an additional contribution towards your care costs, applied if your financial resources are above certain thresholds.

Will I lose my inheritance due to aged care costs?

The aged care system is designed for individuals to contribute to their care based on their financial capacity. While significant assets may be used to pay for care, and ongoing fees can reduce your estate, careful financial planning can help manage these costs and potentially preserve some inheritance. It is important to seek professional advice to understand your specific situation.

Is the family home always counted in means-testing?

Your family home is generally counted as an asset in the means test, but there are specific rules and exemptions. For example, if a protected person (like your partner or a dependent) lives in the home, it may be exempt or valued up to a capped amount. It is important to get advice on your specific circumstances.